What Should I Do if My Business is Facing Bankruptcy?

March 15 2024

Facing bankruptcy is a daunting prospect for any business owner. In the UK, insolvency cases have seen a steady rise in recent years, with over 17,000 corporate insolvencies reported in 2023, according to data from the Insolvency Service.

If your business is teetering on the brink of bankruptcy, it’s crucial to take swift and decisive action to navigate this challenging situation.

Here’s a comprehensive guide on what steps you should take if your business is facing bankruptcy.

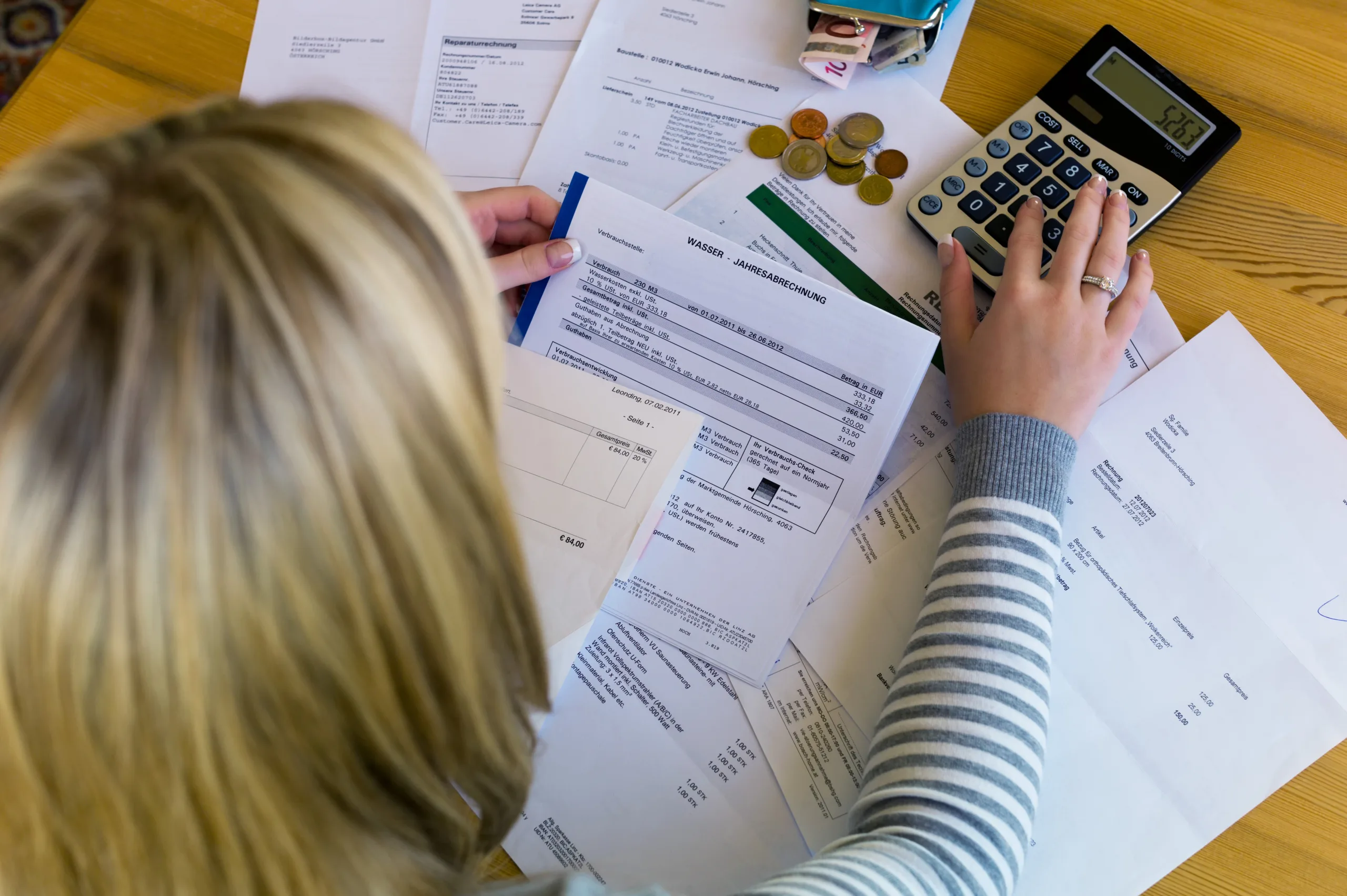

Assess the Financial Situation

The first step in addressing bankruptcy is to conduct a thorough assessment of your business’s financial situation. This includes analysing cash flow, debts, assets and liabilities.

Understanding the root causes of financial distress will enable you to make decisions about the critical next steps to take. A business may face bankruptcy due to various factors, including:

- Mismanagement of finances

- Declining sales or market demand

- Excessive debt burdens

- Unexpected economic downturns

- Disruptive industry trends

Factors such as legal issues, ineffective strategic planning, intense competition or failure to adapt to changing consumer preferences can also contribute to financial distress.

Seek professional advice from accountants or financial advisors to gain clarity on your business’s financial position. For instance, you might look at paying off certain debts first to ease the burden and then trying to arrange longer term repayment plans for other debts.

Consider Company Voluntary Arrangement (CVA)

A Company Voluntary Arrangement (CVA) is a formal agreement between a company and its creditors to repay debts over a fixed period while continuing to trade.

A CVA can provide breathing space for the business to restructure its finances and regain stability. Seek advice from insolvency practitioners to assess whether a CVA is a viable option for your business and to facilitate negotiations with creditors.

Explore Turnaround Options

Declaring for bankruptcy should be considered as a last resort. Before making any decisions, explore potential turnaround options to salvage the business.

This may involve restructuring debts, renegotiating contracts, selling non-core assets or seeking additional funding.

Given that a lot of startups fail, it is not surprising that it might lead to bankruptcy. But they may be simple opportunities to merge with competitors, bring in a new partner with preferential rates or sell the company, especially if you have something of value such as stock, orders or a strong brand.

Engage with turnaround specialists or insolvency practitioners who can provide guidance on restructuring strategies specific to your business’s needs.

Explore Administration

Administration is a legal process that allows insolvent businesses to be restructured or sold as a going concern. It provides protection from creditor action while an administrator takes control of the business to assess its viability and explore restructuring options.

Administration can offer a lifeline for businesses facing imminent bankruptcy by providing an opportunity for a fresh start under new ownership or management.

Liquidation as a Last Resort

If turnaround efforts prove unsuccessful and the business is no longer viable, liquidation may be inevitable.

Liquidation involves selling off assets to repay creditors and winding up the business. There are different types of liquidation procedures available in the UK, including voluntary liquidation (solvent or insolvent) and compulsory liquidation initiated by creditors.

Seek legal advice to navigate the liquidation process and fulfill your obligations as a director.

Seek Professional Advice

Navigating bankruptcy proceedings can be complex and overwhelming. It’s essential to seek professional advice from qualified experts who specialise in insolvency and restructuring.

Insolvency practitioners, solicitors and financial advisors can provide guidance based on your business’s specific circumstances and help you understand the implications of different courses of action.

Communicate Transparently With Your Stakeholders

Effective communication is key when facing bankruptcy. Keep stakeholders, including employees, suppliers, customers and creditors, informed about the situation and any decisions that may impact them.

Transparency builds trust and can help mitigate potential fallout from insolvency proceedings.

Work closely with your appointed advisors to develop a communication strategy that maintains goodwill and minimises disruption to stakeholders.

Take Proactive Steps

Facing bankruptcy is undoubtedly a challenging and stressful experience for any business owner. However, it’s essential to approach the situation with a clear head and take proactive steps to address financial distress.

By exploring your options and seeking professional advice, you can navigate bankruptcy proceedings effectively and emerge stronger on the other side.

Remember that seeking help early can increase the likelihood of finding a viable solution and securing the best possible outcome for your business and its stakeholders.